Condo Recovery Underway and Likely to Accelerate

How to Ride the Wave This Time Around Without Losing Your Shirt

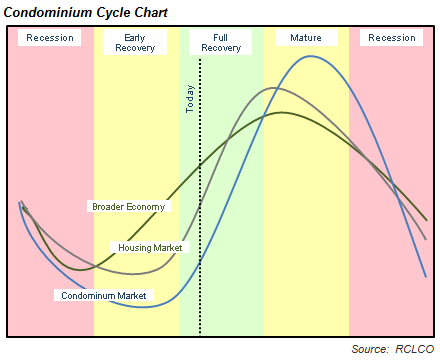

If there’s a single lesson from the recent real estate recession, it’s that history tends to repeat itself. Or as Mark Twain famously said, if it doesn’t exactly repeat itself it sure does seem to rhyme. The specific rhyming we are talking about here is the intensity of the condominium market cycle and the significant opportunities and significant risks posed by participating in this high-beta asset class.

RCLCO’s market outlook is that much like in the 1980s, 1990s, and 2000s, 2014 and for two to three years to follow will be a period of dramatic growth in volume of condominium transactions combined with significant upward price movement caused in part by the lack of available supply in most major urban markets.

These positive market conditions will last for the remaining years of the for-sale housing market recovery while the industry aggressively moves to service this need both with conversions of existing apartment buildings and increasingly new development. This will unfold as delivery of new projects financed as apartments (“switches”) first and purpose-built condo buildings thereafter. This shift will also have the benefit of reducing pipelines in the for-rent multifamily space, where several years of rapidly increasing rents have primed the marketplace for condominium activity.

While this shift is largely cyclical in nature—meaning that it will come to an end as the market becomes saturated and demand begins to ebb with the broader economy later this decade—there are also structural changes underway that will support and amplify the condominium resurgence this time around, and will probably make the sector less prone to contraction with the broader economy. These structural changes include renewed interest in urban or walkable neighborhoods among some household types and the related growing acceptance of high-density housing, the aging of the Baby Boomers, delayed marriage and child rearing among Millennials (Generation Y—see August 8, 2013, RCLCO Advisory), and so forth.

The tenure shift toward rental as opposed to homeownership, however, does not appear to reflect structural changes in preferences. Though economic realities faced by Millennials in particular (student loan debt burdens, higher unemployment rates, delayed wealth creation, and so forth) are real, many studies, including RCLCO’s own research (see sidebar), suggest that the desire for homeownership is as strong as it was for previous generations.

Consumer Research

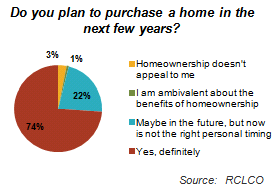

RCLCO is regularly called upon to design and execute consumer research to answer questions regarding program, target market, and positioning. High-density for-sale housing has been a focus of this practice in recent months, and one recent survey focused on affluent young households (ages 25-35) in the D.C. metro area. Questions regarding interest in homeownership—condominiums in particular—yielded particularly interesting insights into the young professional market.

Highlights include:

- Even among affluent young renters, the desire to purchase a home is as strong as ever. Nearly 75% of this group plan to purchase a home in the next few years.

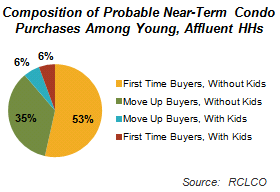

- Probable condo buyers (those definitely or probably considering a condo as their next purchase) are predominantly households without kids, but are by no means all first-time homebuyers. As much as 40% of total condominium activity within this cohort might be buyers moving up within the condominium market.

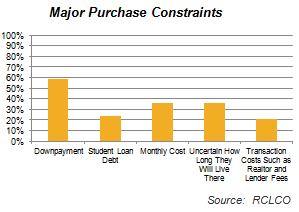

- Few “hard” financial factors appear to be major purchase constraints. While there has been much discussion about the impact of student loan debt, fewer potential purchasers indicated this would be a challenge than were concerned about more traditional issues such as down payments.

As the industry begins to process this opportunity, we are

counseling our clients to:

- Move Wisely, but Quickly—When careful analysis demonstrates an available market with income levels appropriate to support the planned product offering, and a project scaled to the market’s size, respond early in the cycle without being distracted by potentially higher future values as the market escalates. When the cycle turns down it will do so quickly and unsparingly. Similarly, monitor the market. You will inevitably call the peak too early, but the wrenching pain of last cycle’s “so, we’ll lose money on the last deal” strategy cannot be forgotten.

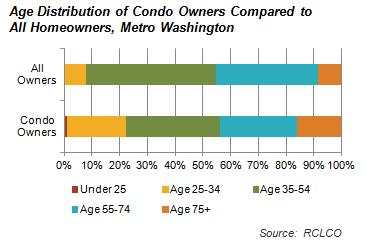

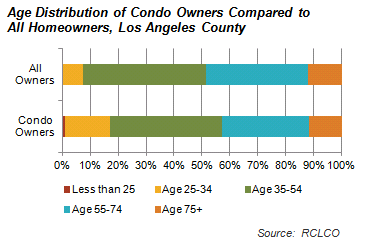

- Don’t Underestimate the Diversity of the U.S. Condominium Market, Think About Market Segmentation—While largely comprised of one- and two-person households (i.e., few kids outside of New York City), condominium buyers span the full age spectrum. The snapshot of high-end condominium owners in Washington and Los Angeles in the chart below is fascinating, the age distribution of condominium owners is remarkably similar to the for-sale housing market overall. In fact, in many established condominium markets the so called “Never Nesters” in their 30s and 40s have been the most active segment. A smart condominium launch entails a careful market segmentation strategy including laser-like feature and amenity design. Resist the temptation to be all things to all people and focus on serving a specific customer.

- Carefully Balance Scale and Marketing Expense—Condominiums, perhaps more than conventional for-sale housing, can have “breakaway performance” due to buzz, or the excitement of the new new thing. The key to rapid and sustained absorption is a strong sense of urgency to purchase, which is best created by scarcity of product. Projects with 100-120 units or less provide, if positioned correctly, a precious and fleeting opportunity (which usually cannot be sustained for more than 18-24 months). Further, budget generously for marketing—3% to 4% of total projected revenues, above the costs of sales and commissions. You can actually buy traffic, but it’s expensive.

- Have HOA Issues Buttoned Up and Rely on Developer Track Record to Address Purchase Objections—Believably communicating true carrying costs will be critical in overcoming cost concerns, and seasoned developers will need to convincingly demonstrate their track record to achieve required presale levels. If anything is different in this cycle, it may be that the close is harder and the customer has better access to information.

- Manage the Balance Sheet—Historically the industry has managed cash backwards, meaning that as the cycle matures the debt being carried (by condominium developers/converters in particular) has increased. Consider using maximum allowable leverage for condominiums today as we believe there are several years left to this for-sale housing upturn, but increase cash reserves and lower debt levels annually over the next three years as the market begins to mature. Cash on hand will allow smart operators to double down on marketing efforts and/or better incentivize buyers when markets ultimately soften to avoid getting caught with half-sold projects.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us