A Warehouse Demand Primer

Logistics Operations Aim for Efficiencies in Time and Cost

Maersk, the world’s largest shipper, recently completed the first of 20 new Triple E ships. The Triple E is the biggest ship ever built. At 1,312 feet long, it is nearly as long as the Empire State building is tall, and it can carry 18,000 TEU (20 foot equivalent units)—or more than 182 million iPads. These ships will operate between China and Northern Europe, but are typical of the increasing sizes of ships throughout the world. U.S. eastern seaports such as New York, Baltimore, Miami, Charleston, Savannah, and Norfolk are scrambling to update and dredge ports to accommodate the post-Panamex ships due by 2015, which have a 12,000 TEU capacity, a nearly three-fold increase over the current 4,500 TEU capacity. Efficiency is the name of the game here, and in this case the Triple E was intended to be 16% larger and 30% more fuel efficient than the largest vessels currently in service. This means significant cost savings for shippers worldwide.

Meanwhile, as the rest of the country was slowly recovering from the 2008 global capital market meltdown, Amazon has been building mega-warehouses of a million square feet or larger in locations such as Phoenix, Nashville, Greenville, and Richmond. E-commerce sales now account for 5.5% of retail sales, up from 4.9% a year ago; and while Amazon has been experiencing revenue growth of 30%+ per year since 2008, average U.S. retail sales were up by only 3% per annum. As e-commerce continues to gain market share, the distribution of goods is increasingly bypassing retail storefronts in favor of direct distribution. Transport speed is thus imperative for shippers who are competing with drive-to retail locations that can be quickly accessed by buyers.

What do these new mega models mean for warehouse demand? In a race for efficiency, the global logistics model is continuously changing. The new patterns of distribution, often involving multiple locations and modes of transportation, will have an impact on both the volume and types of demand for U.S. industrial buildings. Geographically, some markets are more prone to changing distribution patterns, while others will remain more dependent on their local economies.

Goods are Stored near Large Population Bases with Multiple Transportation Modes

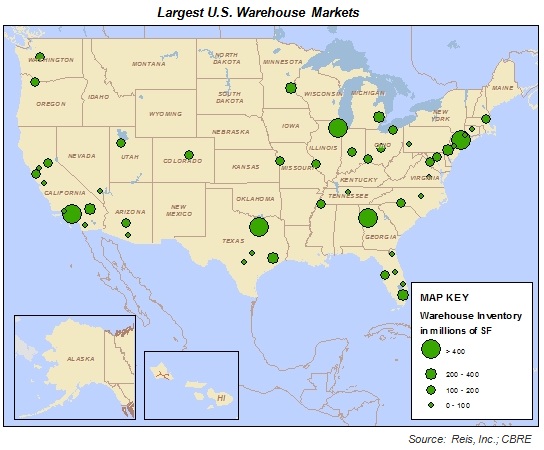

Goods are generally stored near large population bases, particularly those that have significant manufacturing sectors. This allows manufacturers and retailers to minimize both costs and the time needed to move goods. The largest warehouse markets in the country are close to large population concentrations and at the center of the prime trucking routes. The five largest markets (Northern New Jersey, Chicago, Atlanta, Dallas-Ft.Worth, and Los Angeles-Riverside) account for about 35% of institutional quality U.S. warehouse space and 44% of demand during the past five years.

However, large and densely populated areas generally have high operating costs, which is not optimal for the manufacturing and storage of goods. Thus, the movement of goods from one location also has a significant impact on the amount of industrial space needed in a metropolitan area and the configuration of the warehouse location and space.

Trucks Are by far the Most Commonly Used Mode of Moving Goods

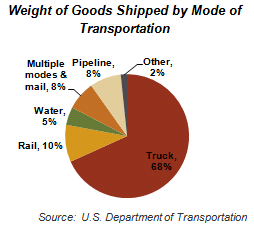

While there are multiple modes of moving goods, trucks are by far the most commonly used. More than 11 million of the 16 million metric tons of goods shipped in the U.S., or 68% of the weight of goods moved, are by truck, with only 10% moved by rail and 5% moved by water.

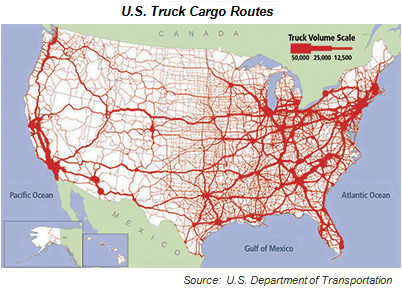

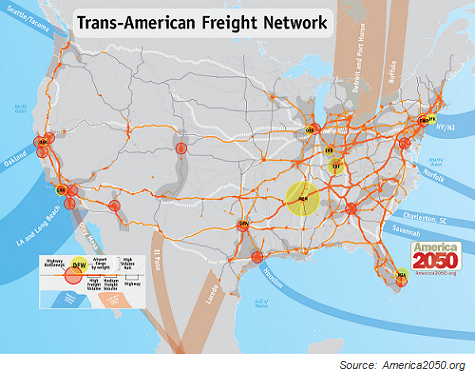

The map below shows the amount of cargo volume moved by highway. Note that the biggest warehouse markets are close to large population bases as well as spokes of highways that allow easy transportation to these population bases in a variety of directions.

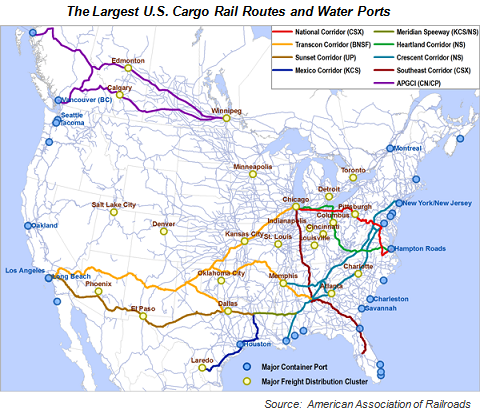

Rail routes (below) are important for some markets. While rail accounts for about 10% of goods shipped and 12% of U.S. warehouse space, many of the products shipped by rail are not stored in institutionally owned warehouses—such as coal, which accounts for 43% of shipment weight by rail.

Goods shipped by water also include a large volume of goods not typically stored in institutional warehouse portfolios, including oil (25% of weight shipped by boat), petroleum, iron ore, coal, and grain. Additionally, containers can be moved directly from ship to rail, thus bypassing the warehouse.

Air transportation is generally used for high cost, low weight items such as mail, electronics, food, and apparel. The largest U.S. air cargo ports include Memphis (FedEx), Anchorage, Louisville (UPS), Miami, Los Angeles, Chicago, New York, and Indianapolis (FedEx). Markets that are dominated by FedEx or UPS may also attract e-commerce retailers that can ship quickly via air or road in these markets. In other markets with large air cargo airports, high throughput facilities that consolidate smaller shipments into larger ones for shipping and then the reverse upon landing may favor low-ceiling, cross docked facilities over the high clear-heights of facilities that are needed for longer term storage. Thus, the transportation mode in the local market can affect both the type of tenant attracted to the area as well as the typical warehouse configuration.

Distribution Needs Determine Warehouse Demand and Space Configuration

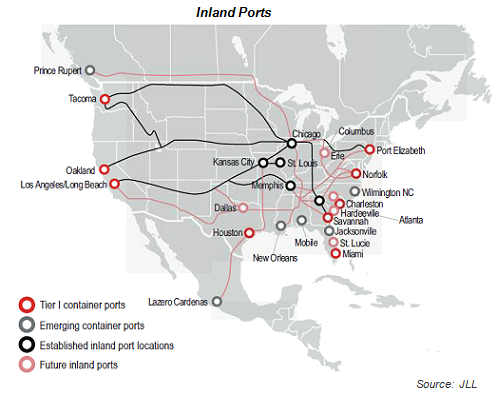

Overall, the national shipping network (below) is constantly innovating to get goods to consumers cheaper and faster. It is also increasingly integrated with global trade patterns. Markets that have the most potential for stable demand are those that have multiple modes of cargo transportation as well as proximity to large population bases (shaded areas in Figure 5). For example, while Savannah and Charleston have significant water ports, they do not have large population bases or warehouse inventories. Conversely, the Oakland water port, which handles less cargo traffic than Savannah, has a larger population base and warehouse sector.

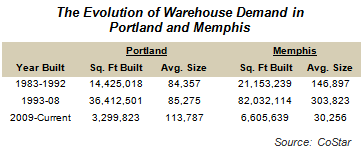

Thus, RCLCO warehouse demand models take into account both the demographic and economic surroundings of industrial buildings as well as modes of transportation. In addition to estimating the volume of demand, significant consideration must be given to the types of buildings that will be supported given the nature of the distribution and storage needs of the local warehouse market. Portland, OR, and Memphis are good examples of medium-sized cities with very different warehouse needs. While the Memphis population base of 1.3 million persons is much smaller than Portland’s 2.3 million, Memphis has nearly twice as much warehouse space. In addition, warehouse buildings in Memphis are on average twice the size of those in Portland (Figure 6). Why is this? Memphis is home to the national distribution hub of FedEx and the largest cargo airport in the country. In addition, it has relatively low costs, ample land and access to multiple highways that are within a one-day drive to a large percent of the U.S. population. Memphis is also located near state borders, which creates competition among states to attract jobs, and thus tax incentives for industrial tenants that further lower warehouse occupation costs.

Thus, RCLCO warehouse demand models take into account both the demographic and economic surroundings of industrial buildings as well as modes of transportation. In addition to estimating the volume of demand, significant consideration must be given to the types of buildings that will be supported given the nature of the distribution and storage needs of the local warehouse market. Portland, OR, and Memphis are good examples of medium-sized cities with very different warehouse needs. While the Memphis population base of 1.3 million persons is much smaller than Portland’s 2.3 million, Memphis has nearly twice as much warehouse space. In addition, warehouse buildings in Memphis are on average twice the size of those in Portland (Figure 6). Why is this? Memphis is home to the national distribution hub of FedEx and the largest cargo airport in the country. In addition, it has relatively low costs, ample land and access to multiple highways that are within a one-day drive to a large percent of the U.S. population. Memphis is also located near state borders, which creates competition among states to attract jobs, and thus tax incentives for industrial tenants that further lower warehouse occupation costs.

Similarly, while access to railroads may not be important in some markets, rail access is key to other markets, both large and small. Some examples are inland ports to which goods are shipped directly from boat by rail. These markets are structured to redistribute large volumes of goods from water ports, are generally located close to large population bases, and have Class I railroads (often with double-stack capacity), foreign trade status, relatively low costs, government-provided tenant incentives, and available labor.

Overall, while warehouse buildings are often considered generic big boxes, the intricacies of each market make them highly specialized environments for the tenants in that market. From a development opportunity perspective, RCLCO ranks target markets for warehouse demand by a number of factors, including the population base within a half or full day’s drive; manufacturing and transportation modes including road, rail, air, and water; and factors such as cost and local government incentives. Markets that score highly have both a large population base that creates a local need for warehouse storage and distribution, as well as key transportation nodes that create demand for regional and national distributors. These markets continuously create high volumes of warehouse demand and include hubs such as Los Angeles-Riverside, Chicago, Dallas-Ft. Worth, Atlanta, and the New Jersey-Philadelphia area. These regions also tend to have a high volume of new construction. Markets that rank low in the path of goods rankings may be good investment markets, but are more likely to be dependent on their local economies for warehouse demand. To be viable as an investment opportunity, these markets should have strong local economic growth expectations. Local markets tend to support smaller buildings, and often have characteristics such as lower clear-heights and proportionately higher amounts of flex space. Other markets that score low in the path of goods rankings may be specialized markets that serve a particular niche in the distribution network. Investors should particularly understand the specialized tenant needs and available tenant incentives in these markets.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us