2024 Looking Better Than Before

RCLCO’s Sentiment Survey has tracked real estate market conditions in the U.S. for over 12 years. The events of the last four years have generated unprecedented volatility in the index – with significant swings in sentiment (both positive and negative) resulting from COVID-19 and the initial recovery; followed by inflation and rising interest rates. The RCLCO sentiment index has remained low throughout 2023 but the future outlook has become more encouraging as we approach the end of the year.

Key Takeaways

- The RCLCO Current Real Estate Market Sentiment Index (RMI)[1], which is measured on a 100-point scale, has remained flat over the past six months ending at 15.47 at Year End 2023, a nominal decrease of just 3.5 from mid-year. The index remains decidedly in the zone that indicates challenging real estate market conditions – an RMI less than 40 is typically consistent with a period of real estate market distress/recession.

- On a decidedly more positive note, a large share of respondents predict that real estate market will be better over the next six to 12 months – the Future RMI is predicted to increase a sizeable 29.7 points to 45.17 over the next 12 months, presaging a rise out of the zone of distress within the next year.

- Also on the rise, a growing share (29%) of respondents believe a national economic recession is unlikely in the next 24 months– although a substantial number believe that we are either currently in a recession (23%), or will be in one within the next year (37%). A smaller share of respondents (11%) believe a recession is more than a year away.

- Among the respondents who believe that a recession is imminent, the majority (72%) anticipate that the recession will likely be of shallow to moderate depth (0% to -2% GDP).

- For most respondents, the for-sale housing market has clearly moved further into downturn in response to waning demand due to high mortgage rates, but sentiment is expected to recover in the next 12 months as rates potentially drop. Most report that multifamily rental housing has moved past the earliest phases of downturn and has entered a full downturn. However, the status of other types of rental housing such as senior CCRC or single-family rentals was more ambiguous, with a similar share of respondents reporting these sectors are either in the stable or downturn phases.

- Beyond housing, looking ahead over the next 12 months, survey respondents expect most of the real estate sectors to be in some stage of downturn, though some niche sectors such as self-storage, lifestyle, and grocery/necessity retail, and industrial are anticipated to have more resilience.

- In another potential sign of optimism, more than half of respondents (59%) predict that inflation will begin to decrease, while 26% believe it will remain the same, and only 15% anticipate that the Fed’s will increase rates further in 2024.

- Respondents expect the homeownership rate in the U.S. will fall in the coming year, which is bad news for homebuilders. However, this will likely continue to drive demand for both multifamily and single-family rentals.

- And a final piece of good news – most market participants expect capital flows to real estate to increase in the coming year.

- Perhaps not surprisingly, office is anticipated to top the list with the largest overall value decline (16.6%) across asset types, with 44% of respondents predicting the decline would be larger than 20%. Other land uses were predicted to decline between 3% and 8% on average

Respondents expect conditions to improve…

The RMI index has had a series of dramatic peaks and valleys during the Covid-19 Pandemic, geopolitical instability, and the Fed’s recent interest rate hikes. RCLCO’s RMI Index in 2021 was exceptionally optimistic reaching a high of 89.1, reflecting an initial wave of confidence in what has been a recovery characterized by fluctuating conditions. Sentiment took a pronounced dive to 8.5 at Year End 2022 – and has remained low ever since. The Fed’s interest rate increases have slowed inflation; but the real estate market is still impacted by higher interest rates, the increased costs of construction financing, and reduced debt availability. These actions are reflected in the current RMI decreasing to 15.5 as real estate markets continue to see slowdowns. However future expectations are becoming more positive (45.1) and represent the highest predictions since the end of 2021.

RCLCO National Real Estate Market Index

Source: RCLCO

The current index at 15.5 puts the market firmly below 30, a level that is typically coincident with periods of economic distress or recession. Looking forward, respondents predict that the index will increase by nearly 30 points over the next 12 months to 45.1, out of the distress/recession zone.

How Would You Rate National Real Estate Market Conditions Today Compared with One Year Ago?

Source: RCLCO

In the past, market sentiment has seen dramatic peaks and valleys, but since Year-End 2022 it has remained mostly unchanged, and largely negative, as challenging market conditions persist. At Year-End 2023, a majority (80%) indicated that national real estate conditions were moderately or significantly worse when compared with one year ago. Most of those respondents felt that real estate market conditions are moderately worse than last year.

- The outlook for the upcoming year predicts a continued decline. A plurality (44%) of respondents predicted that national real estate market conditions would continue to get “moderately” or “significantly” worse in the next year. However, 35% of survey respondents felt conditions would be improving at Year-End 2023, compared to 29% in Mid-Year 2023.

Browse Past Sentiment Surveys

- RCLCO Real Estate Sentiment Increases Slightly, Risk of an Impending Recession Remains

- RCLCO Real Estate Sentiment Hit All Time Low as Recession Looms

- Real Estate Market Sentiment Dips into Recessionary Zone Amid Economic Uncertainty

- Despite a Slight Decline, Sentiment Regarding the Real Estate Market Remains Strong

- Explore ten years of results from all Sentiment Surveys

12-Month U.S. Real Estate Market Predictions over Time

Source: RCLCO

Recession Forecast

A majority (71%) of respondents feel that a recession will occur at some point in the next two years, down from 84% at the 2023 mid-year survey. However, more than half (60%) believe that this recession will occur within the next year. While most of the respondents feel that a recession will occur, just 5% believe the severity will be greater than a -2% decrease in GDP. RCLCO’s Macroeconomic POV projects GDP growth in 2024 between 0% and 1%, more optimistic than the majority of respondents.

When Will the Next U.S. Recession Occur?

Source: RCLCO

What Do You Believe the Depth of Recession Will Be?

Source: RCLCO

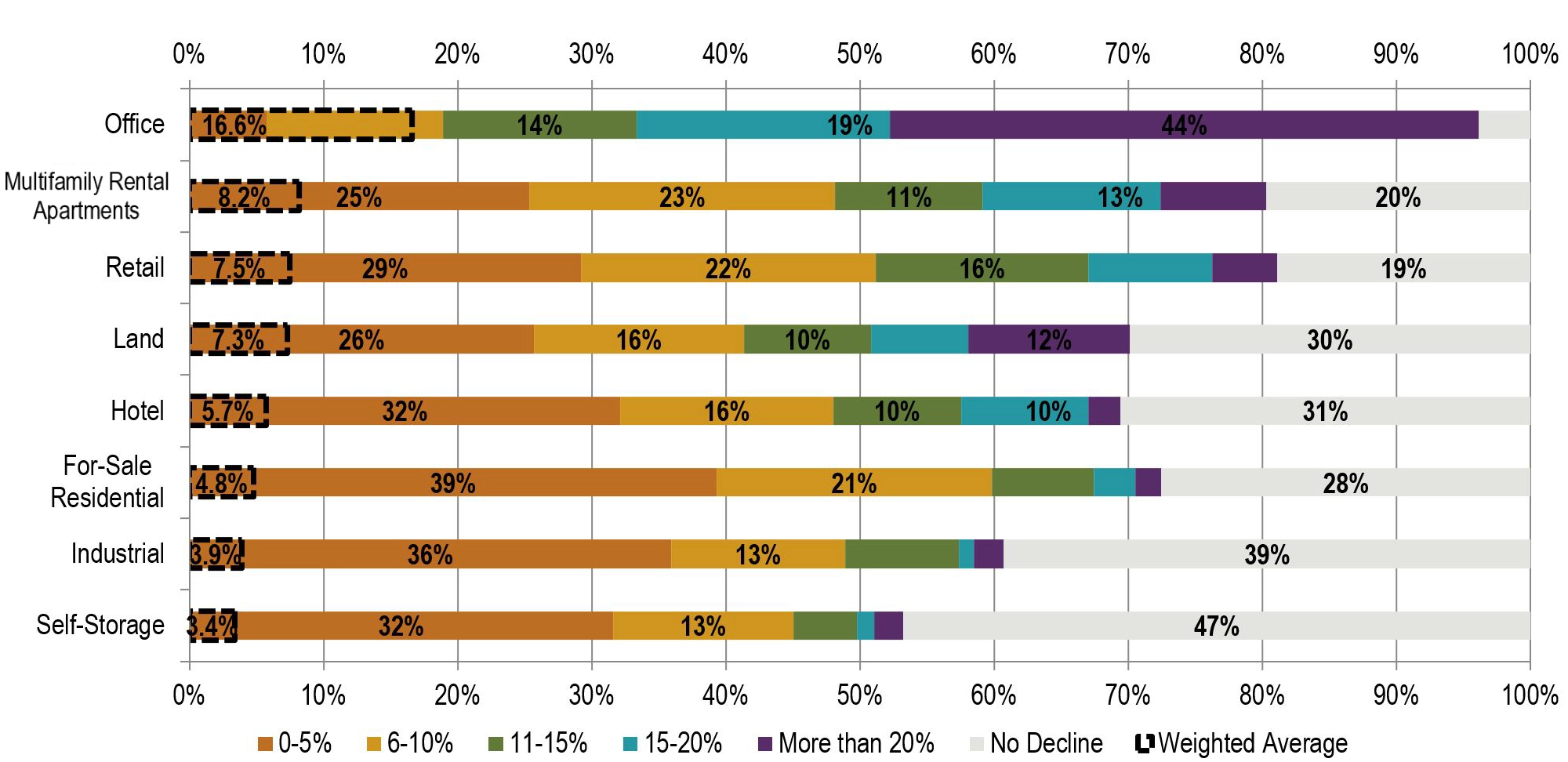

Peak-to-Trough Asset Value Declines

Real estate values have been impacted by current market conditions, and for the wild card question we asked respondents to estimate the peak-to-trough decline of each asset type. Office was the sector that respondents felt would decline in value the most; with over 40% believing office values will end up at 20% below peak, with a weighted average drop of -16.6%. Multifamily was second at -8.2% average decline, followed by retail (-7.5%) and land (-7.3%). However, it is important to note that it can be challenging to tell the whole story with national averages as certain asset classes and geographies are outperforming others based on more nuanced local conditions.

How Far Do You Think That Real Estate Values Will Decline Peak-to-Trough in the Current Cycle?

Operating in the Red

At the end of 2023, we are continuing to experience stress and corrections in the residential real estate sectors. As with our previous survey, we reflect the range of responses (when there is less consensus) in the chart below – the longer the bar, the larger the variation in responses. Commercial uses have more variation since they contain more subsectors of varying performance than the residential groupings, and that detail is labeled on the chart. Sentiment around the for-sale residential sectors was similar among different product types, and most respondents felt it is either well into full downturn, or at the bottom of the cycle. Multifamily rental has moved past peak generally, though subsectors such as single-family rental, age restricted, or seniors housing may still be in stable phases or just entering the early downturn phase. Industrial appears to have remained in the expansionary phases, and hospitality has moved out of downturn into recovery. Retail and office show more variation as grocery/necessity retail and life sciences/medical office outperform other subsectors.

Cycle Stage Movement over Past Six Months

- Residential for-sale uses including Resort/Second Home, For-Sale Homes, Land, and Condo are in downturn. Elevated mortgage rates continue to impact pricing potential and the overall volume of sales.

- The Multifamily apartment sector has entered full downturn, but sentiment regarding more niche rental residential uses such as Age-Restricted Rentals, Single-Family Rentals, and CCRC had less consensus than at Mid-Year 2023. The number of respondents who indicated that these niche sectors remain stable was relatively equal to the number who reported that these sectors are in downturn.

- Retail sentiment varies by subsector. Grocery/Necessity retail sectors performed the highest, with the majority of respondents reporting that they were in early or late stable phases. Lifestyle uses had moderate performance, though many felt the sector was moving into early downturn. There was consensus that Regional Malls have moved into full downturn, though we know that Class A centers have outperformed their Class B peers.

- Hospitality has entered recovery– with travel rates having mostly returned to pre-pandemic levels.

- Office also had a mix of opinions depending on the subsector. Life Sciences/Medical has moved into downturn and shows a more negative view than at Mid-Year 2023. Class B/C office has moved into full downturn, while Class A is approaching bottom.

- The Industrial sector shows signs of moving towards peak, while Self Storage remains solidly in the stable phases.

Many Land Uses Predicted to Move into Early Recovery in Next 12 Months, Some Remain in Downturn

Looking forward, most of the residential sectors are predicted to move into early recovery stages, with the resort/second home market being the least positive. The outlook for commercial sectors is also increasingly positive as grocery-anchored retail, lifestyle retail, storage and data centers, life sciences and medical office are expected to emerge into early recovery. Recovery in sectors such as traditional office, regional malls, and resort/second home residential is expected to lag behind other sectors, remaining in downturn in the coming year.

Economic Indicator Predictions for the Next Year

The 10-Year US Treasury (UST) peaked at nearly 5.0% in mid-October but has since decreased to 3.9% (as of December 2023). Economists and futures markets expect that the UST will hover in the 3.5% to 4.0% range for the next several years. Unlike in past recessions, the Fed is unlikely to lower short-term rates in the near term.

Respondents to the RCLCO survey also weighed in on interest rates; and other real estate factors such as cap rates, capital flows, home ownership and construction costs. For some of the factors at Year End, there was a shifting of opinions from mid-year, but less consensus remains on both cap rates and construction costs.

What Do You Expect to Happen with the Following Economic Indicators Over the Next 6 to 12 Months Nationally?

Source: RCLCO

- The majority (53%) of respondents said that interest rates will decrease at a moderate pace, and 35% predict that interest rates will remain the same. This represents a large shift in expectations, as the majority of respondents in Mid-Year 2023 expected rates to increase, compared to 11% at the end of 2023.

- End of year cap rate forecasts closely follow those from Mid-Year 2023. 35% predicted an increase, 24% predicted a decreased, and 35% predicted them to stay the same.

- Inflation had some of the highest consensus of all the metrics this survey round. The majority (54%) believe that inflation will decrease moderately, 26% believe it will stay the same, and 12% feel it will increase moderately.

- Compared to Mid-Year 2023, opinions have shifted more positively related to capital flows to real estate, with a greater number expecting an increase.

- Construction costs had relatively mixed views, with 32% expecting cost decreases and 31% expecting cost increases.

- A majority (78%) of respondents believe that the homeownership rate will either stay the same or fall, as rising interest rates and low inventory continue to constrain the for-sale housing market.

Where Do You Think the 10-Year Treasury Will be 24 Months From Now?

Source: RCLCO

RCLCO POV

The RCLCO Base Case (70% probability) assumes that the US economy will slow materially in early 2024, with moderate job losses and a recession still possible, although a soft landing seems more likely than just a few quarters ago. Although the 3Q 2023 fears of a broad economic downturn haven’t materialized, most real estate sectors have been experiencing recession-like conditions over the past year with continuing downward pressure on operating fundamentals and values. The possibility of continuing Fed action to squash inflation could tip the economy into a shallow recession in late 2023 or early 2024.

ECONOMIC CONDITIONS

US GDP growth to end 2023 stronger than anticipated at (1.5% to 2.5%) with slowing between zero and 1.0% predicted in 2024. Depending on inflation and geopolitics, the U.S. economy will likely return to trend (2%-3%) growth in 2025. Job growth will moderate to 2.5-3.0 million (annual) in 2023 though is expected to decline in 2024 to zero to 1.0 million, possibly turning negative for parts of the year. As the economy slows, US real estate fundamentals will continue to soften, with moderately higher vacancy rates and slower rent growth in most property types.

- Rental Housing – Demographics, limited for-sale housing inventory, and high borrowing costs will keep multifamily and single-family rental demand strong, although significant supply is slated to come to market over the next 12-18 months and rent/price increases are moderating. Elevated vacancy rates and potential job losses could cause additional softness in the market. Apartment rent growth will struggle in 2024, trending toward 3% thereafter.

- Industrial – Supply is up but vacancy rates should remain low, and demand should stay strong as e-commerce continues to expand and re- and near-shoring accelerate, with rent growth averaging 5% annually through 2026.

- Single-Family – For-sale prices expected to be flat through 2026 and single-family rental (BTR) should continue to gain share of new construction.

- Neighborhood Retail – Rent growth will average 2-3% over the next 3 years as new supply is minimal.

- Niche Sectors – Health care (medical office, life sciences, senior housing), data centers, and self-storage out-perform in recessions and have strong long-term demand drivers.

- Caution is recommended for office and discretionary retail, as ongoing structural shifts create greater risk. Net effective office rents will contract 1-2% annually, and vacancies will hit new highs, approaching 20% by 2026. Deep discounts in some cases will create some opportunistic buying/redevelopment opportunities

- Once land prices adjust, strong fundamentals and long-term growth support selective development and refurbishment of rental residential, industrial, and some niche property types (life science, medical office).

Real estate capital markets to remain constrained in 2024 as lending is tight and borrowing costs have risen materially. Institutions are constrained by valuation uncertainty and potential recession impacts, although wholesale selling is unlikely. Transactions may pick up in late 2024 once buyers adjust to reset prices (20% to 40% below peak, depending upon the asset class). The public real estate markets are very bearish, with implied cap rates much higher than in private markets.

Values for many sectors will likely fall below replacement cost, creating buying opportunities, although many office and retail properties may have limited future usefulness. Widespread distress is not expected, except for office and non-dominant regional malls.

Job growth in gateway markets is forecasted to rebound, although Sunbelt markets will continue to outperform.

Who Took the Survey?

RCLCO’s Real Estate Market Sentiment Survey tracks the sentiments of a highly experienced pool of real estate professionals from across the country and the industry. A majority (68%) of respondents have worked in the real estate industry for 20 years or more, with an average respondent tenure of approximately 25 years, and 81% of respondents are C-suite or senior executives in their organizations.

Years of Experience in Real Estate

Source: RCLCO

Position in Organization

Source: RCLCO

Developers and builders comprise the largest share of respondents, at 47% of the sample. Another 18% are investors or capital allocators, followed by 4% in design or architecture firms. The remaining 30% of respondents come from a variety of other types of organizations within the real estate industry and public sector.

Type of Organization

Source: RCLCO

The respondent mix is representative of the U.S. as a whole: however, it is weighted towards those who report working primarily in coastal and Sunbelt markets. This respondent mix reflects markets where there has been significant development activity in this cycle.

Primary Region/Market

Source: RCLCO

Sentiment Survey article and research prepared by Charles Hewlett, Managing Director; Kelly Mangold, Principal, and Scott Cottier, Analyst

References

[1] The Real Estate Market Index (RMI) is based on a semiannual survey of real estate market participants and is designed to take the pulse of real estate market conditions from the perspective of real estate industry participants. The survey asks respondents to rate real estate market conditions at the present time compared with one year earlier (Current RMI), and expectations over the next 12 months (Future RMI). The RMI is a diffusion index calculated for each series by applying the formula “(Improving – Declining + 100)/2.” The indices are not seasonally adjusted. Based on this calculation, the RMI can range between 0 and 100. RMI values in the 60 to 70+ range are indicative of very good market conditions. Values below 30 are typically coincident with periods of economic and real estate market stress/recession.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Copyright ©️ 2023 RCLCO. All rights reserved. RCLCO and The Best Minds in Real Estate are trademarks of Robert Charles Lesser & Co. All other company and product names may be trademarks of the respective companies with which they are associated.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us