The Big Shrink: The Shift Toward Smaller Industrial Spaces in the Face of Growing User Demands

E-Commerce’s Effect On Industrial

E-commerce continues to fundamentally redefine the real estate sector. The industrial space, specifically, has seen a paradigm shift both in where industrial product is being located as well the types of product demanded. As customer expectations for delivery timeframes compress, e-commerce is reshaping the industrial fulfillment and distribution network itself, with locations of facilities depending relatively less on proximity to ports and more on distance to consumers and dense population bases. As such, over the last several years, three types of facilities have emerged as the building blocks of modern distribution systems:

- Regional mega distribution centers: Highly automated facilities, typically comprising over 1 million square feet, in strategic locations based on (1) land availability, (2) transportation infrastructure (including seaports), and (3) proximity to consumer bases.

- Mid-sized distribution centers located at the market edge: Distribution centers located near major arterial routes outside large cities that are largely automated and cross-docked to facilitate the quick transfer of goods.

- Small, urban warehouses for last-mile delivery: Smaller warehouses that serve as the last point along the distribution chain before delivery. These facilities range from 10,000 to 150,000 square feet, feature less automation, and are located in urban environments near population centers.

Amazon, in particular, has been a bellwether for the future of distribution center demand. For example, even as it continues to operate and develop dozens of one million square foot mega distribution centers nationally, the company has opened 25 “sortation” centers of approximately 300,000 square feet since 2014. These centers are located in the suburbs of major markets and sort packages by zip code for final delivery.

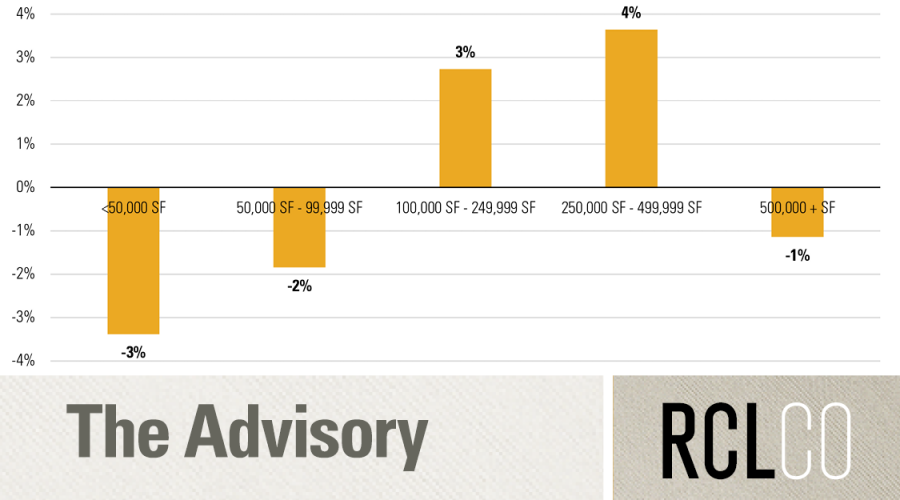

Demand Shifts for Smaller Space

Over the past few years, online-only retailers have rapidly expanded their exposure while traditional brick-and-mortar stores have aggressively retooled their retail strategy to capitalize on the new consumer demand for expedited delivery. This has resulted in growth in demand for smaller industrial facilities in urban locations. While the shifts above have been documented ad nauseam, the figure below illustrates that the size segment with the largest increase in requirements was the 100,000-249,999 square foot segment.

Size Requirements by Number of Total Active Tenants Touring the Market

SOURCE: JLL U.S. Industrial Market Report

Construction Is Slow To Respond

Despite increased demand trends for last-mile and urban warehouses, construction activity is concentrated in buildings with at least 250,000 square feet.

Deliveries by Size 2010-2016 YTD

SOURCE: Costar

Change in Share of Deliveries 2010-2016 YTD

SOURCE: Costar

Why Is Construction Lagging?

If the demand for industrial space has been shifting toward smaller “last-mile” distribution space, why has supply failed to meet these needs?

The “last-mile” strategy dictates the need for the industrial space near major population centers where developable land is already scarce. The real challenge becomes pronounced in larger cities, where millennials are increasingly making a larger proportion of their expenditures through online retail, and developable land is in great demand for more higher and best uses such as multifamily or retail.

Additionally, construction activity has remained concentrated in buildings with at least 250,000 square feet located outside of large cities due to the excessively high costs of construction and lack of availability of urban infill locations. Urban warehouses have specific needs, including loading docks and ceiling height requirements, that limit potential locations for urban infill.

With developable land already at a potentially infeasible premium, one possible option for industrial users in need of urban industrial is the redevelopment of existing space. Because large big-box retail space has, perhaps, been hit the hardest by the recent e-commerce trends, many of these large big-box spaces have now been rendered functionally obsolete. While it would be expensive to retrofit these spaces, many are ideally located in dense urban settings where the demand for industrial space is most difficult to meet. As e-commerce trends continue to dictate the need for more “last-mile” delivery space, the renovation of existing retail space may become a more common and feasible option.

Article and research prepared by Simon Soomekh, Vice President, and Kyle Ruane, Associate.

RCLCO provides real estate economics and market analysis, strategic planning, management consulting, litigation support, fiscal and economic impact analysis, investment analysis, portfolio structuring, and monitoring services to real estate investors, developers, home builders, financial institutions, and public agencies. Our real estate consultants help clients make the best decisions about real estate investment, repositioning, planning, and development.

RCLCO’s advisory groups provide market-driven, analytically based, and financially sound solutions. Interested in learning more about RCLCO’s services? Please visit us at www.rclco.com/expertise.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us